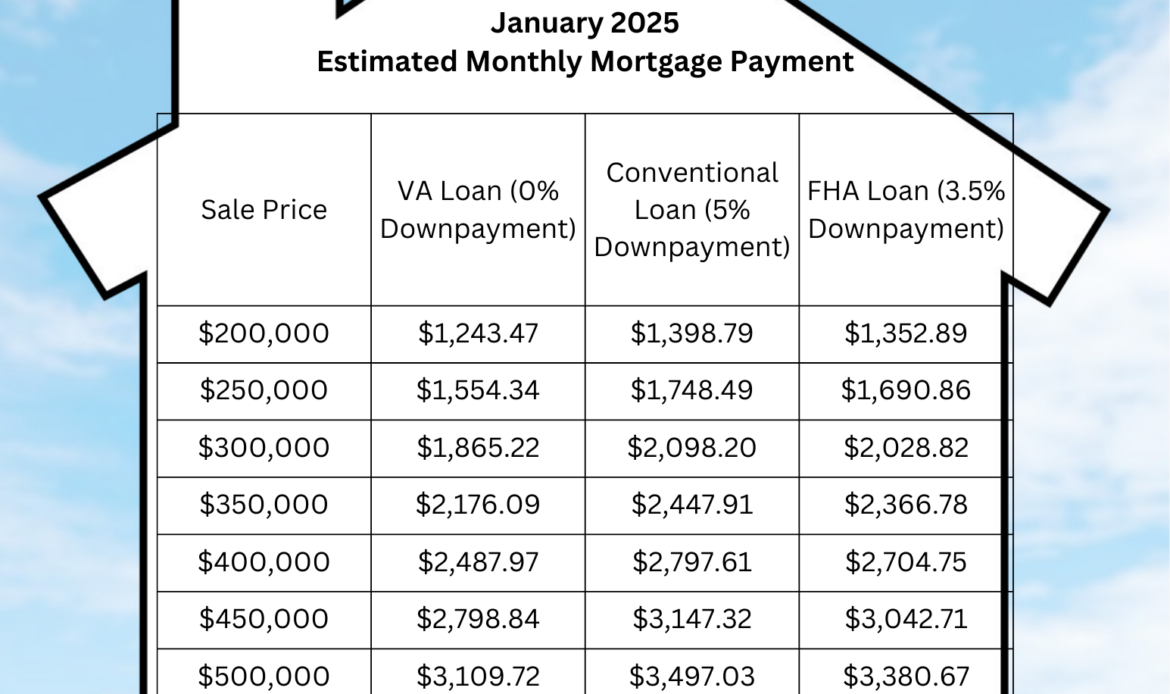

Here’s a table showing estimated monthly mortgage payments for different loan types and sale prices, assuming a 30-year fixed-rate mortgage and the 6.25% interest rate.

Renting in 2025? Should you buy or keep renting? It’s a complex question. In my opinion, if your TOTAL rent expense is less than $1,200 per month, stay there as long as possible and stack your savings to invest soon.

If you are in a position like my recent buyer client and were told that at the end of your lease, your monthly rent for an “ok” apartment was going up by $500 per month, you had some savings towards buying expenses, a good credit score, and plan to be in the area for at least the next 5 years… all signs are pointing towards buying.

Breakdown:

– VA Loan: No downpayment, so the loan amount equals the sale price. The monthly payments are generally lower than those of the other loan types due to no downpayment requirement.

– Conventional Loan: 5% downpayment, so the loan amount is 95% of the sale price. This results in a slightly higher monthly payment.

– FHA Loan: 3.5% downpayment, so the loan amount is 96.5% of the sale price. FHA loans tend to have a similar monthly payment to conventional loans but might come with additional insurance costs (MIP) which aren’t accounted for here.

Notes:

– These are estimates for the principal and interest portion of your mortgage payments only.

– The actual total mortgage payment (PITI) would include taxes and insurance, which can vary by location and other factors.

– The FHA loan payments can be higher in certain cases due to Mortgage Insurance Premium (MIP) requirements.